In this week’s MoCo Economy Watch blogpost, we take a dive into… shopping!? Well, Retail anyway. More precisely, how the County’s retail is connected to state & local revenue and our economic development aspirations.

A premature obituary for brick-and-mortar retail

It seems like every week or two there is a new article being written about the demise of brick-and-mortar retail. After all, Amazon is now the third largest company in the world. However, even during a year of stay-at-home orders with many stores remaining closed, 80% of retail sales occurred offline in 2020 (and it is reasonable to expect that share to rise a bit this year, as many folks are anticipating a bounce-back). But the future of shopping is a lot more complicated than just brick-and-mortar versus e-commerce.

At-place retail is still highly relevant: it creates a “there there” which helps locations compete for new residents and jobs, it activates street life, it drives traffic and economic activity, and more urgently, represents a large source of tax revenue. Leaving aside Federal aid, Sales and Use Tax represented 16% of the State of Maryland’s total revenues in FY21, approximately half the revenue from Individual Income Taxes. Thus, while jobs and employment are the keys to reviving Montgomery County’s economy, maintaining the County’s share of retail sales is – at a minimum -also important. Unfortunately, based on data from the past few years, the County seems to be losing ground on this as well.

It isn’t about too much space, it’s about not enough sales

The Montgomery County Planning Department commissioned a retail study in 2017 which found that “overall, retail supply across Montgomery County is very well balanced with demand. There is neither the overabundance of retail that characterizes many of our neighboring jurisdictions, not an undersupply.” Given that retail square footage across Europe only works out to about 6 sq. ft. per person, the study made the argument that we’d be more well-prepared and resilient for changes from e-commerce by having less inventory than our neighbors. The study noted that we have about 25 square feet of retail inventory per capita, slightly below the 27 feet per capita for the DC-Baltimore region, and well below several of our regional peers (Prince George’s @ 28 sf per capita; Fairfax @ 29 sf per capita; Loudoun @ 36 sf per capita, etc.).

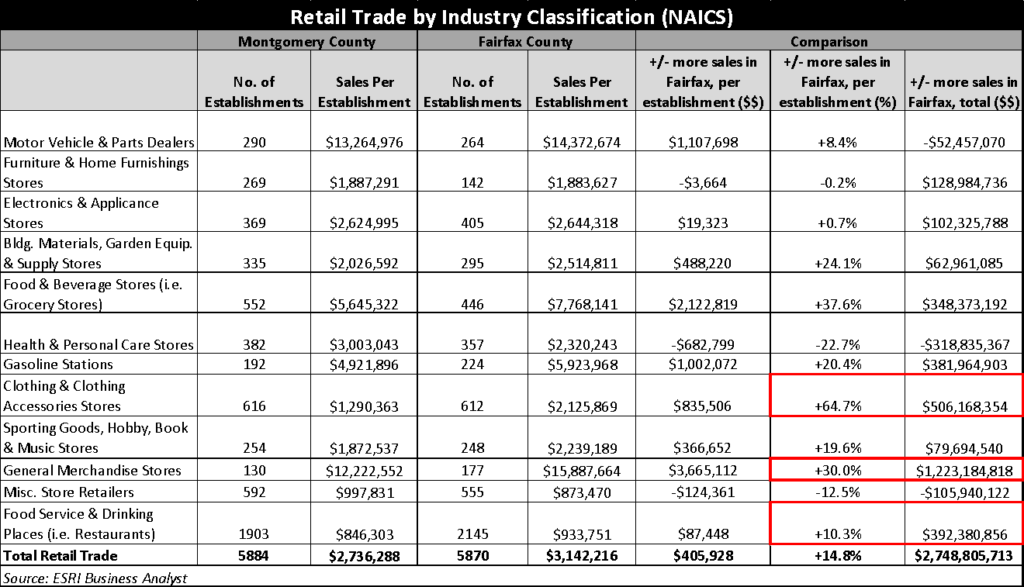

So, um, yay? While we don’t disagree that a leaner inventory better prepares us for the future and we agree that brick-and-mortar retail is facing serious headwinds, the question isn’t really whether the County has too much or too little space. What we don’t think gets enough attention is a focus on the quality and sales productivity of the retail space in Montgomery County. Take a look at the table below, which compares Montgomery and Fairfax County using 2017 at-place (excluding e-commerce) retail sales data.

Based on U.S. Census defined retail categories, the average retailer in Fairfax is earning $400,000 more than in Montgomery County! In fact, in just about every major retail category – other than Miscellaneous Retailers and Health & Personal Care Stores, i.e., your CVS or local hair salon – the sales productivity for the average business is significantly higher across the Potomac. Aside from the County having $2.75 billion less in retail sales to tax than Fairfax, this table brings to light many of the larger challenges to Montgomery County’s business climate as well….

- Operating Margins: An increase of +10.3% in sales for a restaurant isn’t just a bonus; it can mean the difference between life or death for a business in the restaurant industry, which survives on low margins (even more so in the COVID-19 era). While we believe individual restaurants with the best quality, service, and concept in either County will thrive, this data could give anyone looking to open a restaurant in Montgomery County series pause, especially if they’re deciding between Montgomery or Fairfax.

- Retail Leakage: Two other categories of note where retail sales in Montgomery County trail behind is in Clothing (-65% per business) and General Merchandise (-30% per business). Why draw attention to these categories? These two types of retail are what we call “Shoppers Goods”, the kind of products people are willing to drive longer distances for to compare price, quality or variety, such as by going to Tysons Galleria or Reston Town Center (in contrast, you wouldn’t drive there for a gallon of milk!). What we suspect is happening here may be “retail leakage” from other places; in other words, more people from Montgomery and Prince George’s County are shopping for these types of goods in Fairfax then the other way around. Not only does Maryland lose disposable income to Virginia in this scenario, but more importantly, these retail nodes become reinforced as the locations where people and businesses want to congregate, thereby attracting a disproportionate amount of the new business investment in the region.

This is why Fairfax County, despite already having more retail space per capita, continues to have lower retail vacancy rates than Montgomery County (3.4% vs. 5.2%, per CoStar). Frankly, a lot of the challenge for Montgomery County is how little new retail has been developed in recent years – for example, since 2017 Fairfax County has added twice as much new retail – 1.2M sf versus 0.6M sf. In fact, the only major new retail project in recent Mo Co history is the Clarksburg Premium Outlet project which represents a really large share of what has been built in the County over the past decade. Most retail is developed with planned (or at least anticipated!) obsolescence in mind, so a healthy retail pipeline is critically important.

This has been going on for a few years

Even if we concede that we’re losing retail expenditures to Fairfax, the harder reality to face is that we’ve been falling behind even our in-state counterparts. The table below shows growth rates of Sales & Use Tax collection over the past 5 years, including and excluding E-commerce sales (which is taxed only at the State level).

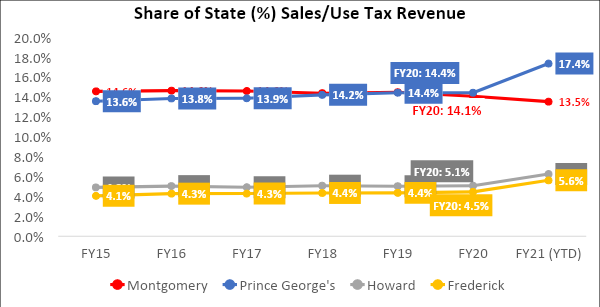

First off, it is encouraging to see that while year-over-year sales tax growth exclusive of e-commerce is either small or occasionally negative for many jurisdictions, sales tax inclusive of e-commerce is fairly steady and positive for both Maryland and Virginia, suggesting that it can be a stabilizing factor to the tax base. Just seeing how Maryland’s at-place sales tax declined 6.2% in 2020 -while sales tax inclusive of e-commerce grew at 1.0% during the same time – is evidence enough for now. But back to Montgomery County. Recently, Montgomery County has experienced the most sluggish retail sales of any nearby Maryland jurisdiction. This is true for both the Pre-Pandemic period (2016-2019) and through FY21-to-date, with cumulative growth rates of +4.0% and -27.2%, respectively (a blog entry for a different day could analyze the impact of pandemic-related closure policies, which were different from county to county). Regardless, its difficult to say with a straight face that Montgomery County’s performance is in line with its neighbors; 2016-2019 sales tax revenue grew 0.6% less than the state as a whole, and a whopping 5.9% less than a composite of Prince George’s, Howard, and Frederick counties. As a result, Montgomery County is falling behind on its share of sales tax revenue to the state, with one neighbor in particular charging up ahead.

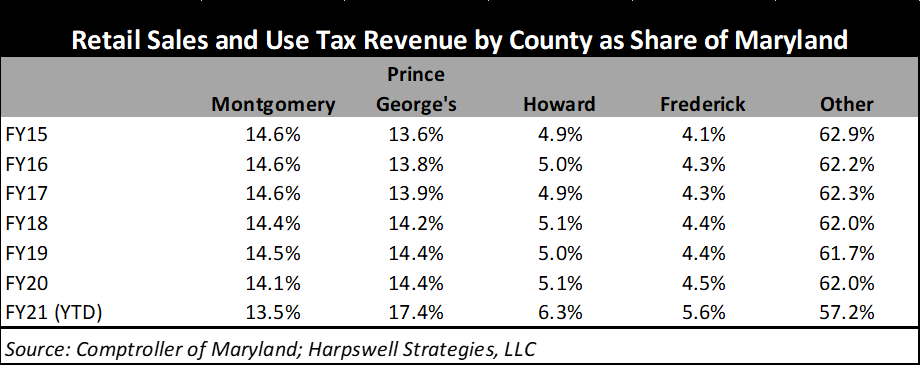

That’s right, according to the Comptroller of Maryland, the share of sales & use tax from Prince George’s County finally exceeded Montgomery County’s in FY20. Prince George’s County had been gradually closing in over the past few years and, over the past year and half, it seems that Prince George’s has passed us by and sped on ahead. Furthermore, while Montgomery County’s other Maryland neighbors appear to be eating into our market share as well (Mo Co’s sales tax quietly declined by 0.5% between FY15-FY20, while an almost equivalent amount (+0.6%) was picked up by Howard County and Frederick County during that period.

This retail and real estate stuff is such a drag!

Literally.

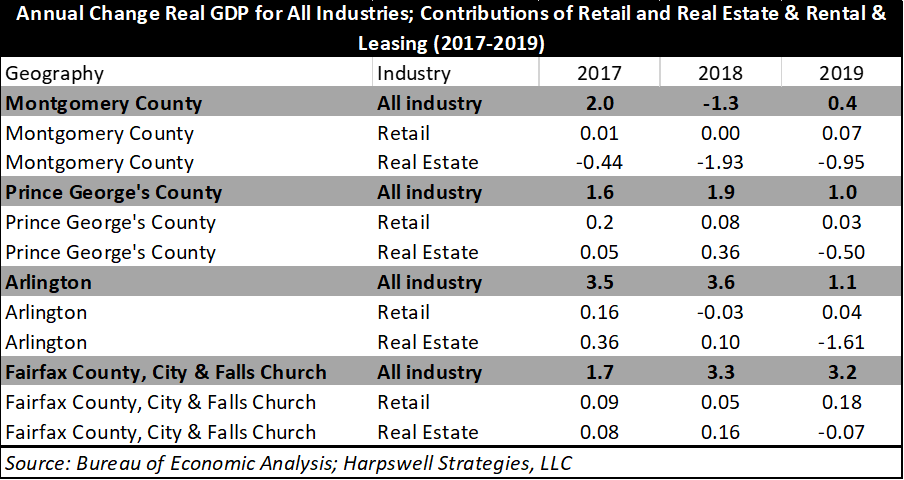

Even before the pandemic, Montgomery County’s overall economy was losing out on potential growth because of this increasingly obsolete and stagnant retail and real estate environment. From 2017 to 2019, Montgomery County overall was seeing less value-add from the real estate sector than its neighbors, and the real estate & rental & leasing industries had become a real drag on the County’s economic growth. Obviously, what we hope is that the pandemic does not act as the accelerant for a broader and steeper decline. As the table below illustrates, real estate & rental & leasing actually dragged County real GDP growth into the red over two consecutive years (2018 and 2019), while retail did little on its own to change the picture and generally did less for our economy than it did in nearby jurisdictions.

Some final thoughts

We’ll want to keep a close eye on where things settle once the pandemic moves into our rearview mirror, but we can’t stop thinking and planning in the hopes that future data releases will vindicate our current position.

- It is too reductive to blame empty storefronts and declining retail sales solely on online shopping. There clearly are other things going on, and there are many areas that are still within our control to improve – most notably, the business climate.

- Current and recent problems are not the result of retail vacancies. Rather, the decline of Montgomery County retail appears to be related to not enough new retail development and not enough economic dynamism – we need a healthy retail pipeline and more robust local business formation.

- When high-income jobs meet well-designed retail clusters with high caliber tenants – be it a Pike & Rose, Tysons, or Reston Town Center – it is like a virtuous cycle that gets the economic flywheel spinning to the point when it can be propelled by its own momentum. We need more of those high-end jobs…and some shopping destinations for those workers to splurge in.

- Outside of the Clarksburg Premium Outlets and Federal Realty’s Bethesda Row and Pike & Rose, what Montgomery County retail destinations are actually pulling consumers from around the region? Friendship Heights, in spite of investment and re-positioning, seems to be struggling to compete with high-end competition in downtown DC and Tyson’s Corner. Silver Spring’s CBD seems to be backsliding and over the past couple of years has lost its signature employer. These places take decades to create and an unwavering commitment across different administrations… where are those places today in Montgomery County and what public policy levers can we pull to boost the health of the retail in those locations?

We’ll back soon with some odds and ends. In the meantime…be well, and shop Mo Co.