In this edition of Mo Co Economy Watch, we provide an update on recently released 2021 GDP and Personal Income statistics. The numbers illustrate that the region is capturing a shrinking share of national growth. After adjusting for inflation, Mo Co’s economy is still smaller than it was a few years ago. That said, the numbers show that 2021 was more positive for Mo Co than other recent years. Real estate and construction continue to be a drag on the local economy. Retail struggles continue to reflect the dramatic shift in income levels of in-movers. Government continues to not really drive much of anything in the local economy, which doesn’t detract from the stability that it provides but continues to call into question the validity of the “proximity to the federal government” narrative in local economic development.

2021 GROSS DOMESTIC PRODUCT

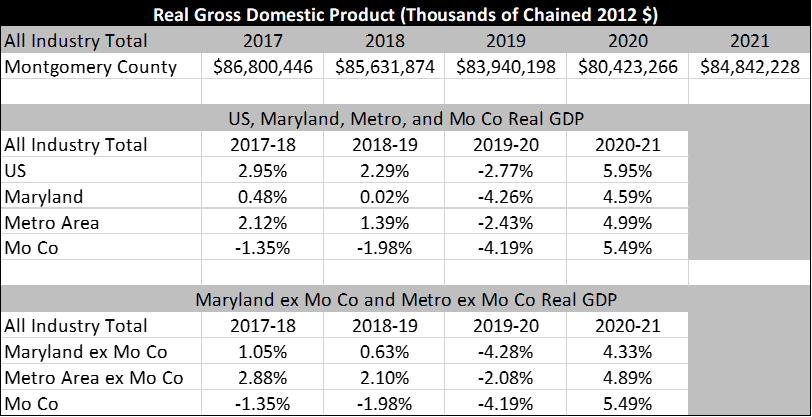

Last year’s local GDP numbers have been released. This data becomes available almost a full 12 months after the end of each year, so it is not useful as a real time indicator but is very valuable for putting trends into perspective and providing context for how the machinery of the economy works.

First, let’s start with the headlines: (1) Mo Co real GDP increased at a rate that was faster than both the state and the Metro region in 2021, though below the national growth rate; (2) Mo Co real GDP remains below the level in 2016, meaning that after accounting for inflation the Mo Co economy is smaller than it was 5 years ago. In current dollar terms, Mo Co GDP increased by 8.2% from 2020 to 2021, while the inflation-adjusted increase was 5.5%.

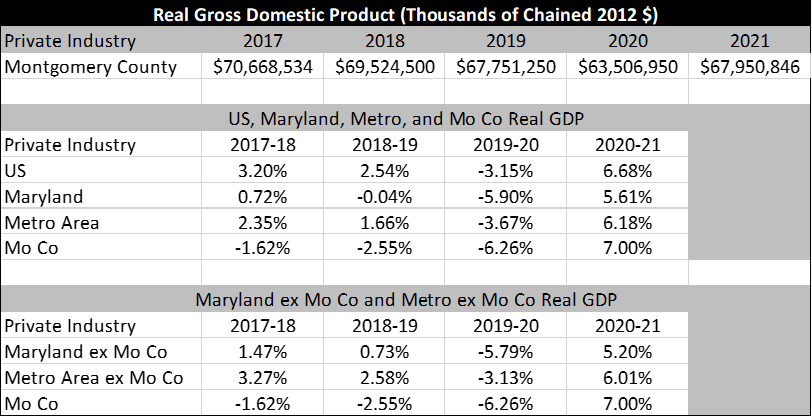

The private industry GDP numbers tell a similar story. Mo Co outperformed both the state and the region in 2021, after several years of underperforming.

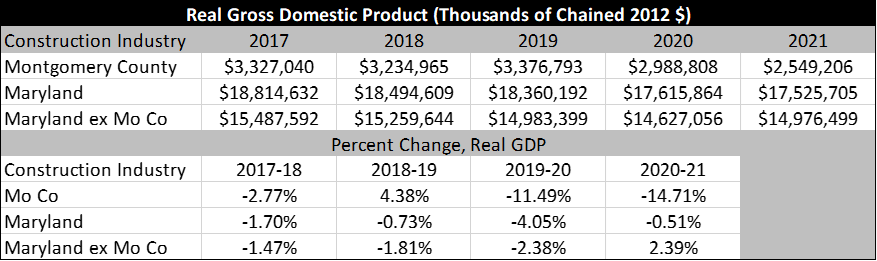

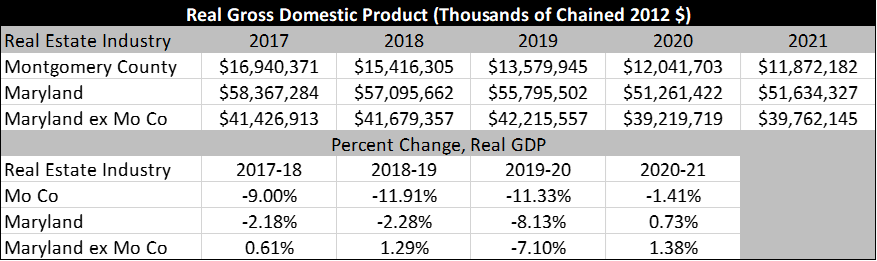

As usual, what stands out when you look at the industry breakdown is that Mo Co’s real estate and construction industries are really struggling. The value-added output of the local construction industry is 23.4% below where it was in 2017, and the value-added output of the local real estate industry is 29.2% below 2017 levels.

To put those declines in perspective, nationally the construction industry has grown by 2.2% over that time, and the real estate industry has grown by 6.4%. If those industries had grown at the same rate locally as they did nationally, the Mo Co economy would be an astounding 8.2% larger than it currently is.

Mo Co has been a significant drag on the County’s economy and on the economic performance of those industries in Maryland. Most likely, the lack of activity and investment in real estate and construction will have longer-term consequences in the form of fewer competitive office and retail spaces, neighborhoods that are less attractive to residents on-the-move, etc.

Here are some other notable facts from the real GDP data:

- Retail trade in Mo Co was up 2.2% in 2021, above the 1.9% for the metro region, but below the 3.1% increase for Maryland and 2.6% increase nationally.

- Professional and business services were up 9.3% compared to 2020, and this set of industries was not hit particularly hard by the pandemic. This is very good news, though the local growth is well below the 11.7% national growth rate.

- Similarly, the information industry had a very strong year in 2021, up 47.7% from 2020. This industry had been a long and steep decline for more than a decade, so this is a very good sign. On the other hand, Mo Co GDP in this industry is still below 2017 levels.

- Manufacturing real GDP increased by 4.8% in 2021, below the U.S. growth in the industry of 6.7%.

- Accommodation and food services GDP was 18.7% above 2020 levels, but don’t get too excited – the industry is still below pre-pandemic levels, and the local growth came in well below the 26.2% growth at the national level.

- Government and government enterprises grew at 0.03% locally, below the recent average annual growth rate of 1.1% and well below the national growth rate of 5.4%.

In the “things-we-tell-ourselves” category, one thing we frequently hear is that Mo Co’s key assets are “proximity to the federal government” and “our talented and educated workforce.” Those assets have not been driving growth in the local economy. If proximity to the federal government were particularly valuable, we’d see it in things like growth in the government’s contribution to GDP…or in Mo Co outperforming the competition when it comes to industries that include a lot of government contractors. Mo Co’s competition is mostly local, and within the region those attributes aren’t special – for example, the Mo Co growth rate in the professional and business services industries was 9.3% in 2021, while the industry grew 10.3% in the rest of the state…even though Mo Co is both more educated and closer to the federal government than most of the rest of Maryland.

2021 PERSONAL INCOME

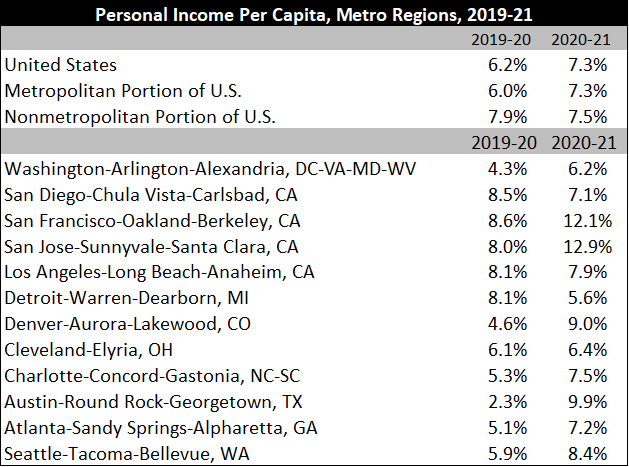

Personal income data for 2021 is also now available. The top line numbers are impressive: U.S. personal income increased by 7.5% in 2021. U.S. per capita personal income was up 7.3% for the year in 2021. Overall, non-metro personal income (+7.5%) increased at a slightly faster rate nationally than did the personal income in metropolitan areas (+7.3%). The Washington-Arlington-Alexandria (DC-VA-MD-WV) metropolitan area experienced an increase of 6.2%, placing it 270th on the list of U.S. metro areas. Below is a non-scientific cross section of some peer metro areas:

So, again, the D.C. region has not been capturing a large or growing share of national growth. There isn’t much regional growth to go around, and the County has struggled to compete with its regional peers for that shrinking share of growth.

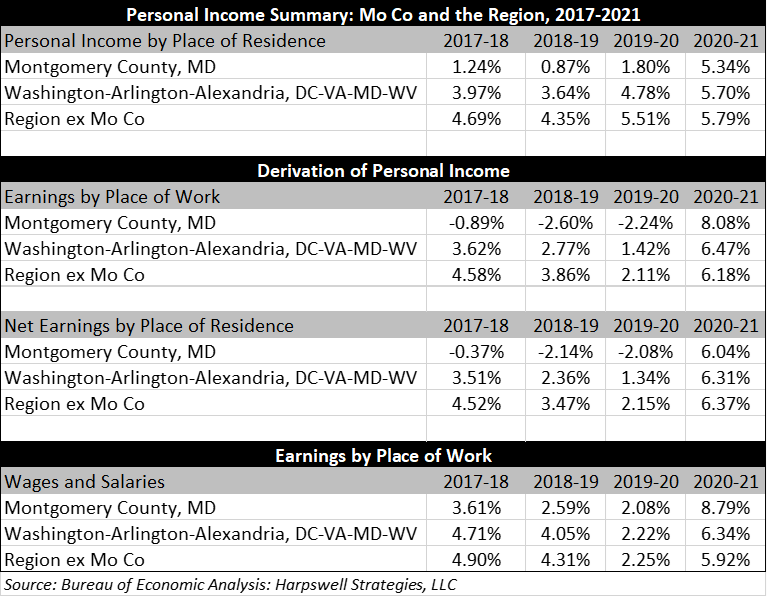

At the County level, personal income by place of residence increased by 5.33% in current dollars. On a per capita basis, personal income increased by 5.98%. That sounds good, but of course the reason that per capita personal income increased at a faster rate than personal income is that the county population decreased by 6,416 from 2020 to 2021. Just to state the obvious, if the sources of economic growth generally are labor force size and labor force productivity, then at a minimum losing population indicates that it is unlikely that the community is growing its labor force. In terms of a breakdown between the two, labor force growth is about 20% to 25% of total potential growth, with the remainder coming from productivity improvements. Personal income by metro area is generally consistent with that, with higher rates of personal income growth in locations that are seeing labor force gains (generally, the U.S. south and west).

Without question, the bright spot in the 2021 data is an increase of 8.8% in wages and salaries by place of work compared to 2020; that increase is much higher than the 6.3% increase in wage and salary income for the metro region. This followed up much smaller gains of 3.6% from 2017 to 2018, 2.6% from 2018 to 2019, and 2.1% from 2019 to 2020. The big 2021 gains helped Mo Co catch back up with the rest of the region – the compound average annual growth rate in wages and salaries for those working in the metro area was 4.3% from 2017 to 2021, while Mo Co is now back within striking range at 4.2% over the same timeframe. So, a very good year but it is just one data point, and it takes more than one to make a trend.

From 2020 to 2021, metropolitan area net earnings by place of residence increased by 6.3%, somewhat higher than Mo Co’s 6.0%. However, that Mo Co is within striking distance of region here is a positive sign given the compound annual average growth rate over the period from 2017 to 2021 – even with some signs of strength in 2021, Mo Co net earnings by place of residence has only averaged a 0.3% annual increase compared to 3.4% for the metro region.

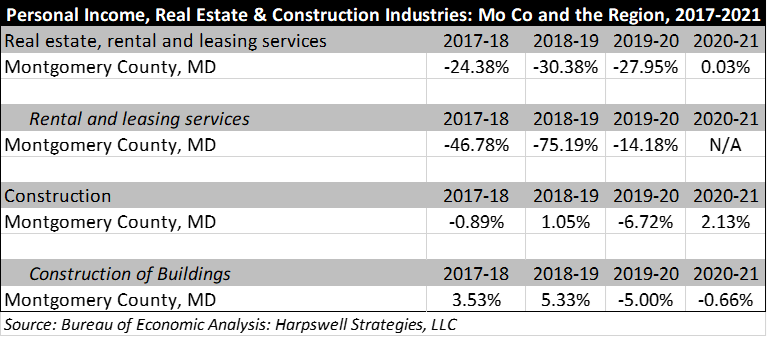

In terms of the factors driving local change, one that jumps out is real estate and rental and leasing services, which has declined from 7.9% of Montgomery County personal income in 2017 to 2.7% in 2021. Looking at this differently, Mo Co personal income increased by $8.5 billion from 2017 to 2021 but would have increased by about $13 billion annually if real estate and rental and leasing services had simply remained constant.

Getting a “little more micro” in focus, the rental and leasing services industry has seen personal income decrease from $3.2 billion in 2017 to $1.7 billion in 2018 to…about $350 million in 2021. This means that the personal income from rental and leasing services declined by nearly 90% from 2017 to 2021, and by nearly 80% from 2018 to 2021. And yet, rent control legislation…

Furthermore, personal income from construction of buildings is another industry that illustrates the effects of Mo Co’s slo-mo growth. For that industry, the compound average annual growth rate (2017-2021) regionally is 5.3%, compared to 0.7% for Mo Co.

I’ve previously touched on retail, but it is worth noting that regionally personal income from general merchandise stores is increasing at a much slower rate in Mo Co than elsewhere in the region (averaging 1.1% growth per year in Mo Co, compared to 2.4% per year in the region). Again, when a disproportionate share of the growth is low to very low income, there is not much incentive to invest in retail real estate, and when the retail real estate gets stale then people shop elsewhere…even when the shopping is of the “stuff households regularly need” variety.

WRAPPING UP

While my consulting practice tends to focus on the economics of specific public policy issues, I enjoy “opening up the hood” to examine how the marble machine of the economy is functioning. If nothing else, it helps me to understand how policy changes end up affecting the broader economy and the longer-term trajectory of a local economy. If you enjoy these pieces, don’t hesitate to reach out and let me know, and to keep my services in mind when your organization is planning for the future. It helps to have someone who knows how the machine works when you need to figure out what is coming based on what has happened so far.

I have a couple of year-end and look-ahead pieces in the works…until then: be well, stay sane, and shop Mo Co!