Probably! In this edition of Mo Co Economy Watch, we’ll touch on what a recession is, how economists determine whether the U.S. economy is in a recession, think about how to apply that logic to a local economy, and identify the factors that could buttress the local economy in the event of a national and/or global recession. Let’s dig in…

What is a recession?

According to the National Bureau of Economic Research (NBER), a recession is “significant decline in economic activity that is spread across the economy and that lasts more than a few months.” It is often said that we are in a recession when the U.S. economy is experiencing two consecutive quarters of negative real GDP growth (i.e., two consecutive calendar quarters in which the economy, on an inflation-adjusted basis, has contracted); in reality, there is no set formula for determining when the U.S. economy is in recession.

NBER determines whether the economy is in recession after careful consideration of a number of monthly and quarterly datasets that describe U.S. economic activity. In making that determination, NBER considers three key criteria: depth, diffusion, and duration of the economic decline. As such, not all recessions are equal – some may be the result of small but widespread and long-lasting declines, others may be brief but deep, etc. And while quarterly data are certainly part of NBER’s deliberative process, in particular when it comes to determining when a recession begins and ends, most of NBER’s determination is made on the basis of higher-frequency releases such as monthly data related to income, employment, consumption, sales, and industrial production.

If you are interested in reading more on the topic, the NBER’s Business Cycle Dating Committee webpage is a good place to start. You may also want to check out (1) this 2022 Congressional Research Service report on the business cycle, and (2) this White House blog post that explains how economists determine if the economy is in recession.

What are some of the specific factors or tests that economists use when debating whether or not the U.S. economy is in recession?

Most economists and wonks are not satisfied by the tautology that “we’re in an official recession when the NBER’s Business Cycle Dating Committee says that we’re in a recession.” Furthermore, economists are pretty keen to look back and attempt to determine when/how/whether a recession occurred. As such, some potential tests have been suggested and “back tested.” We need not go into a lot of detail, but I’ll describe a few those now.

One two-part test that is sometimes cited requires (a) two consecutive quarters of real GDP decline, and (b) labor market conditions that meet the so-called “Sahm rule”, i.e., a 3-month moving average unemployment rate that is at least 0.5% (50 basis points) above its lowest point in the previous 12 months. Economists who argue that the U.S. economy is not in recession right now often cite the “Sahm rule” as support for the argument. If you are interested, the Federal Reserve Bank of St. Louis has a handy “Sahm Rule Recession Indicator” that you can keep an eye on.

One time-tested indicator that a recession is coming is the so-called “inversion of the yield curve.” The term describes the global bond market conditions that are present when the markets view investing in U.S. government debt over the shorter term (say, the next 2 years) to be riskier than investing in U.S. government debt over the longer term (say, the next 10 years). As you can see below, as between the 2-year and 10-year bonds the curve has inverted. This piece in the New York Times is a good explainer.

Is there an agreed upon method for determining if a LOCAL economy is in recession?

As you might have guessed, there isn’t any single approach to determining whether a local economy is in recession. And given that much of the data reported monthly at the national level is…not reported monthly at a local level…and is reported, if ever, with much more significant lag or delay…there wouldn’t be much point in it. So, all we have to go on is whether or not a national recession is underway. If so, we can look back when the data becomes available to determine whether the timing of the local economic downturn was substantially different from the timing of the national economic downturn.

In light of data limitations and timing issues, how might we think about making a real time determination of local recession?

Here’s where things get tricky. Some data that is available for the national economy is not yet available for local economies – for example, 2022 Q1 and Q2 GDP data is available for the U.S. (and now for states), but this info won’t be available for local economies until late 2023.

First, let’s examine the question of whether there have been two consecutive calendar quarters of declining real (inflation adjusted) GDP. We won’t have County-level GDP or personal income statistics until late 2023, but we can at least look at the U.S. and Maryland numbers for some insights.

- U.S. real GDP declined in both the 1st and 2nd quarters of 2022.

- Maryland real GDP also declined in both the 1st and 2nd quarters of 2022.

Second, we can use the U.S. and Maryland numbers to gain some insights into how the County’s economy might have performed.

- If we apply the performance of each industry at a national and state level to the County’s industry mix, we can see that the County is likely to have experienced a decline in real GDP during each of the first two quarters of 2022.

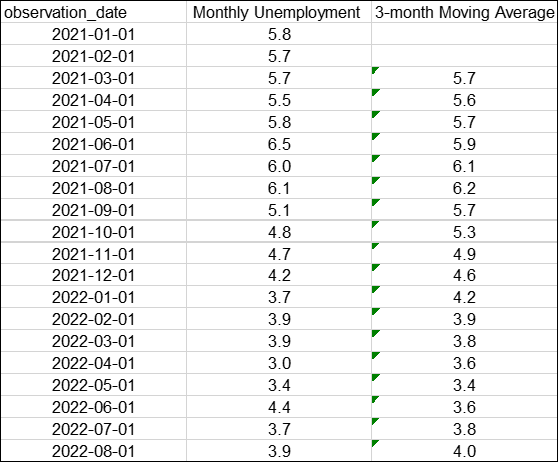

Third, we can apply the Sahm rule to Mo Co specifically – that is, we can compare the 3-month moving average unemployment rate (U3) to the low from the previous 12 months.

- The 12-month low of the 3-month moving average unemployment rate was 3.4% in May of this 2022.

- The current 3-month moving average unemployment rate hit 4.0% in August (the most current monthly data).

- This difference of 0.6% passes the Sahm test (is greater than 0.5%).

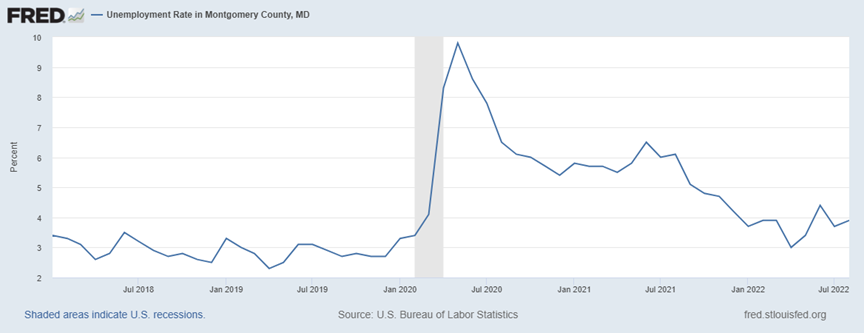

If you want to see a visual representation of the monthly unemployment rate without the smoothing, see the graph below, which illustrates the recent vintage uptick in unemployment.

So, where does Mo Co stand?

Here’s a quick run down of what we’ve covered and how it applies to Mo Co:

- The 2 yr/10 yr yield curve inverted, which indicates that a national recession is very likely in the near term.

- Nationally, the economy has contracted in two consecutive quarters on an inflation adjusted basis.

- However, a U.S. recession has not yet been declared in large part because the U.S. employment market remains strong.

- One condition that has been met locally, but not nationally, is the most often considered labor market criteria of recession: the Sahm rule. In Mo Co, unlike nationally, the unemployment rate has increased meaningfully when contrasted to the 12-month low.

- To the extent that we can tell (due to data limitations) it appears likely that the local economy contracted in both Q1 and Q2. We don’t yet have the local data, but we do have Maryland data. And furthermore, using the performance of each industry nationally and in Maryland to Mo Co’s industry mix, it appears quite likely that the Mo Co economy contracted in Q1 and Q2 along with the Maryland and U.S. economies.

- We don’t need to beat a dead horse, but we know that the Mo Co economy has been stagnant for years and has routinely underperformed relative to the broader regional and national economy and has been losing jobs for…a decade already now.

- If a national recession is declared by NBER, regional economists might reasonably conclude that the recession began earlier in Mo Co than it did nationally.

If the nation does fall into a recession, what local factors might buttress Mo Co?

The County (and the region) are less affected by the business cycle than a lot of places and may be less affected by some of the current economic dynamics.

- The County is helped during recessions by having a large public sector element to the economic base (21.4% of GDP in Mo Co versus 11.6% of GDP nationally).

- One aspect of the current national economic contraction is that business inventories are declining; since there isn’t a lot that is “made in Mo Co,” this shouldn’t affect the local economy as much as it does some others that are more dependent on manufacturing (6.3% of GDP in Mo Co versus 11.3% of GDP nationally).

- Vaccine research and manufacturing is counter-cyclical insofar as demand will be highest when public health pressures on the national and global economy are at their peak.

- The County and the greater DC region are not major exporters, and therefore are likely to be less affected by the havoc that has been caused by the strong dollar making U.S. made goods more expensive to buy abroad. This chart shows that the DC region is ranked 25th among Metro areas when it comes to dollars of exported goods.

Wrapping up…

The big risk is that a wobbling local economy will be knocked into a tailspin by national and global economic forces. However, it is worth pointing out that in Mo Co part of the issue will be how to determine when the current wobbling/stagnation/malaise has become something more acute. This is where economists, if there were a local business cycle dating committee, might start to focus on the “duration” criteria – the downturn need not be deep, or much deeper than it has been, given that the context is a lengthy decline that has resulted in fewer wage and salary jobs in the County today than there were a decade ago.

I’ll be back later this month with a Flotsam and Jetsam…and with another installment on recessions. In that second recession piece, I’ll look at some issues like which local industries are most likely to be affected by a recession, and how and when a recession might affect the County’s budgets. Until then…be well, stay safe, and shop Mo Co!