By Rick Liu, Senior Economic Advisor

As I’ve huddled in the house the past few days as infection levels continue to rise (well, that and 5 straight days of a 100+ degree heat index, mind you), I’ve been thinking about what happened 18 months ago when we hit an intense albeit brief economic downturn. Like previous downturns, I recalled hearing once again the age-old argument for “balanced growth” that went something like this:

Old Perspective: “If we’re in an economic downturn, we should avoid overbuilding because we’re going to have so much vacant office space that needs to be absorbed.”

I’ve always had a great deal of respect for the attention MoCo puts on responsible growth and long-term planning; it is one of the reasons I loved working there. But as well intentioned as this argument is, I never agreed with it. So, in this fictitious conversation I’m having in my head with this person, I’d like to offer a counterargument and a new perspective:

New Perspective: “Actually, a strong commercial pipeline – even in a downturn – is needed not only for us to attract MORE jobs and workers, but simply to ‘run in place’.”

I know what you’re thinking. Building spec office buildings right now is a tall order – even among the strongest job markets – and some you probably think it’s a silly time to be writing about this topic. But assuming we WILL go back in the office at some point, and given how much our working habits have changed a lot in the last 18 months, I actually think it’s the PERFECT time to be having a conversation about this because we will need new office space that’s responsive to our needs once we go back to work.

Office Buildings are not commodities

I frequently tell my spouse we don’t have to buy new Tupperware – old, yellowed-out containers do just as well in keeping food fresh as new ones – but office buildings don’t really work the same way. Here are three reasons why:

- Office Trends Change: I interviewed a senior practice leader at Gensler about the characteristics of competitive office buildings today vs. older buildings (~20+ years). I learned many of the features demanded by top companies are cost prohibitive to retrofit in older properties, both mechanically and architecturally, and often makes more sense to build new. Some features he mentioned were…

- Upgraded HVAC systems bringing in dedicated outside air (requiring full replacement of distribution systems, risers, and equipment on rooftops)

- LEED Gold certification (not to mention legislation for more stringent building performance standards by our own council)

- Rooftop space (notably, rooftops of older buildings are dominated by mechanical equipment)

- Multiple breakout rooms (rather than 1 to 2 executive conference rooms)

- Amenity space (fitness centers, wellness centers, etc.)

- Upgraded HVAC systems bringing in dedicated outside air (requiring full replacement of distribution systems, risers, and equipment on rooftops)

The COMSAT building: Beautiful but empty

To be clear, none of these features are impossible for property owners to install with enough money. However, between the cost of renovations, the subpar quality of a retrofitted solution, and modest rent premium they could obtain as a result, he said that most owners would rather lower the existing rent and wait to build something new from the ground up.

2. Office Location Preferences Change: Despite infill development efforts for the past 20 years and a “return to the city”, we still have a huge inventory of suburban, auto-oriented, single use buildings built in the 80’s and 90’s (which coincidentally was the highwater mark for construction in Montgomery County) that are out of step with the times. To use an extreme example, consider the COMSAT building and the challenges current and recent ownership has faced in finding suitable tenants. The type of places where people want to work and live change significantly over 30-40 years, but office buildings themselves can’t be put on wheels and moved to a new location. Thus, vacancies in undesirable office locations haven’t been shown to relieve demand in desirable locations.

3. Office Jobs Change: And this is really the clincher.This is a “jobs world”, and office buildings are just living in it. In other words, office space needs to conform to the changing nature of work, not the other way around. And boy, have industries evolved over the last 40 years (in contrast, the kind of food stored in my Tupperware really hasn’t changed much). Until the 1980’s, most people’s desk consisted of a typewriter and rotary phone; you’re now more likely to find them at an antique shop or yard sale. While less abrupt, it should come as no surprise that many of our office buildings from 40 years ago are gradually losing their functionality too. Technology evolves, work evolves, and the offices that not only evolve with them but are able to pinpoint future trends and deliver them before they become widespread, are going to be the most successful in attracting the high-income workforce this County is competing for.

But does Montgomery County need more office space?

Even if you’re convinced that not all office space is the same or interchangeable, the question remains whether we NEED more office space (which invariably depends on how you define “need”). For someone who’s always thinking about our economy, the importance to me of having a strong pipeline to me is (surprise, surprise!) laying the groundwork and infrastructure to attract high-paying jobs and industries to Montgomery County in the future who won’t settle for not having their needs met. In that regard, our comparatively weak pipeline has left us with an older inventory and put us at a disadvantage to attract talent firms need to create high-paying jobs.

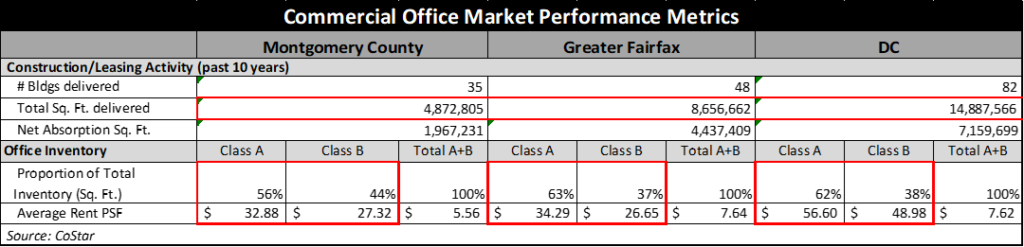

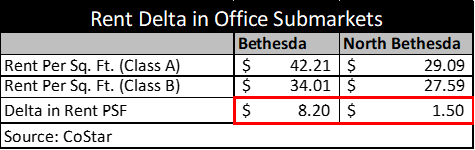

Over the last 10 years, we’ve constructed barely over half the office square footage of Fairfax County (8.6M SF) and less than a third of DC (14.5M SF). What this means for the longer term is that we have a larger proportion of older, Class B space that’s ill-equipped to compete for modern companies that we need to grow our economy. Ostensibly, a little over half of our office stock is Class A, while the ratio is closer to two-thirds for Fairfax County and DC. But it gets worse. Dig deeper, and the delta in rent per square foot between Class A and B is smaller in Montgomery County ($5.56) than Fairfax ($7.64) and DC ($7.62), which signals that much of our Class A space is in name only but doesn’t actually compete in the same realm with trophy office space in Tysons, Reston, or DC. This “delta” in rents is one of the key metrics lending institutions use to underwrite new office projects, which only creates more development interest in Fairfax and DC. This phenomenon can also be observed closer to home when comparing Bethesda to North Bethesda.

This partially goes towards explaining why new office construction has surged in downtown Bethesda over the last few years, while new office construction in White Flint has struggled. Its effect on our economic “flywheel” becomes significant over time, since new construction leads to higher rents, higher-paying tenants, and a wider delta in rents resulting in more lender appetite for new construction in that area. Unfortunately, with capital directed at the most attractive opportunities, it also works in reverse. Stagnant office markets receive less attention and further stagnate, putting pressure on the County to use incentives as a way to catalyze investment and reverse the flywheel’s direction.

Why this Matters

A refrain I often hear is that County shouldn’t incentive commercial construction, because persistently high vacancies are really the property owner’s problem. I completely agree (though, as discussed in a previous newsletter, office vacancies are also a property tax revenue problem), but it’s conflates two different issues. One problem is on the property level, which the owner is responsible for solving usually through “economically rational” decisions that advance their own interest (e.g., lower the rent, make low-cost improvements, sell the property, etc.). The second problem is when the collective impact of all these decisions – although rational on an individual basis – begin to depress the overall state of our economy. Whether or not we agree on who’s responsible for solving the problem, all of us bear the brunt of the impact.

Ultimately, we need to recognize employers that offer well-paying jobs and employ hundreds of people view office space as a valuable asset to help them attract top talent for high-paying jobs, enhance their brand, and conduct their business in a dynamic environment. Because rental costs are modest relative to a successful business’ gross revenue (5%-10% is a rule of thumb), it isn’t in their interest to do it “on the cheap” unless it’s for a back-office function. This is why a healthy office pipeline is so important; the best companies won’t settle for second best to carry out high value activities. Failing to do this means we lose out on not only attracting new companies to the County but also in keeping the ones we have; in other words, we have to “run just to stay in place”. A good example of this is Federal Realty Investment Trust’s recently built 909 Rose office building at Pike & Rose. In an interview I had with a representative from the company, I was told most of their tenants came not from elsewhere in the region, but from within Montgomery County (who also were willing to pay a 15% rent premium in the submarket, a sign of potentially good things to come for North Bethesda). Some may unfairly describe this as “musical chairs” at best or poaching at worst. But if there’s anything you’ve learned from my previous blogs, office users providing professional services have no trouble moving beyond the political boundaries of Montgomery County and even the State of Maryland (unlike retail, whose customer base tends to be local). If anything, Northern Virginia’s comparatively stronger talent base and stronger business environment mean it is IMPERATIVE we have a competitive office stock and pipeline if we want to stay in the game.

Look, I’m not advocating for “office development Reaganomics,” where we should carelessly build as much office product as we can and expect older buildings to “trickle down” to satisfy everyone else’s needs until they become obsolete. Far from it. As I said in the beginning, I do believe in responsible and balanced growth, which to me means accommodating businesses across the spectrum of sizes, industries, and growth stages. What’s clear right now is we don’t have enough office supply to satisfy those at the top, and we are leaving jobs, tax revenue, and future financial flexibility on the proverbial table without a healthy pipeline.