This month, I summarize and provide some context for recent vintage economic data. Specifically, electricity and energy consumption, inflation, and the size of the labor force.

ENERGY

The most recent release from the U.S. Energy Information Administration indicates that (nationally) end use of electricity increased in June and was 6.6% higher than in June 2020. In fact, June marked the 7th consecutive month in which U.S. electricity consumption exceeded consumption for that same month in 2020. On average, total consumption in April-June was 6.0% higher in 2021 than in 2020. The amount of electricity consumed has been buoyed by the return to work.

Energy consumption is a decent, if flawed, proxy for overall economic activity. One of the things that will be interesting to watch this year is whether the year-over-year increase in the commercial sector outpaces the decrease in household consumption of electricity. My guess is that it won’t – even though many people are still working from home, a hybrid work model probably means (net) more electricity used to power work (at home and in offices) than a year ago when most office workplaces were entirely shuttered. I anticipate that the result will be excess fuel/energy tax revenues for the County (above the budgeted amount), though that will of course depend on the mix of residential and commercial usage because fuel/energy sources are taxed at different rates depending on whether they are sold to residential or commercial consumers.

In case you were wondering, skyrocketing natural gas prices will certainly affect residential consumers this year, but because our fuel/energy tax is based on units of consumption rather than dollars/receipts, those prices themselves are unlikely to do anything to boost County revenue. One potentially unanticipated result could be that power plants will continue to shift to consuming more coal. June 2021 coal consumption for producing electricity was 30.8% above June 2020 and 8.5% above June 2019. Ask your lungs if they have noticed a difference!

INFLATION

August inflation data indicates 12-month inflation in the neighborhood of 5.5% (5.3% for all urban consumers, 5.8% for all urban wage workers). That is really high compared to what we have grown accustomed to in this country.

Inflation is what happens when there is a shortage of goods and/or services relative to the amount of money and credit available to buy them. Too much demand or too little supply can both be the cause of inflation. And inflation can take different forms – consumer price inflation, asset price inflation, monetary inflation, etc. Currently, the economy is experiencing monetary inflation. This is what happens when the supply of money increases suddenly and then there is a lot more money chasing an unchanged supply of goods and services. Monetary inflation is what is often referred to as a “demand-pull” inflation, i.e., inflation that is caused by demand for goods and services that exceeds the economy’s capacity to produce goods and services, ergo prices go up.

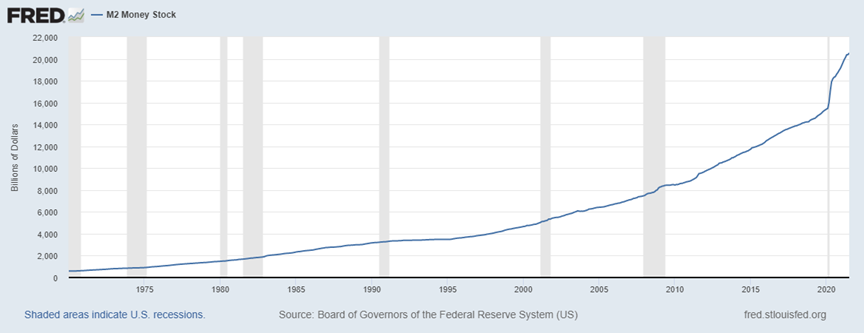

What has been driving inflation recently is a rapid increase in the amount of money sloshing about in the economy. To be specific, the amount of money in the system has increased by 33% since January 2020. Below is a graph showing the supply of money in the U.S. economy (and here I am using “M2” or “broad money” as the measure):

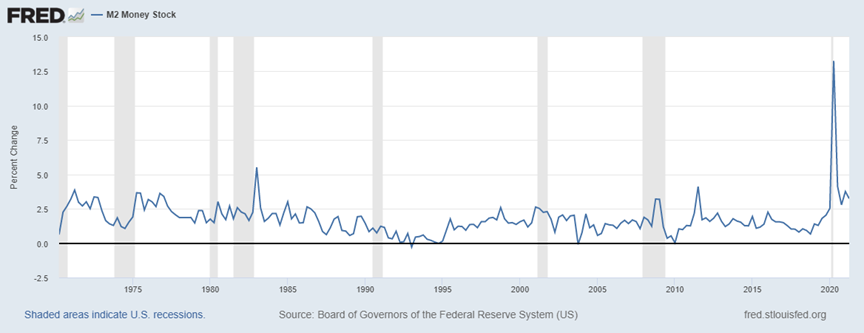

You can see how quickly the supply of broad money changed by looking at the quarterly percentage change graph below. I know we’re all sick of hearing the word “unprecedented,” but there really isn’t another word that is appropriate here.

I think what we are likely seeing is a permanent increase in the prices for a lot of goods and services that goes well beyond anything that we would have expected in the absence of this rapid increase in the money supply. Certainly, some of the current inflation relates to specific supply-chain bottlenecks rather than deficit-funded demand shocks, but it does appear to be mostly a function of the amount of money sloshing around the balance sheets of businesses and households. There will be less sloshing around over time, and for now (leaving aside the congressional democrats $3.5 trillion in potential federal spending plan) it appears likely that this summer was the peak.

LOCAL IMPACTS OF INFLATION

Normally, I’d see a lot of deficit-funded government spending as something that could drive some local economic growth. In this case, I don’t really see a lot of up-side for the regional economy. First, a lot of the recent spending spree has been focused on the household sector (Ben Bernanke’s “helicopter money”) rather than additional spending on existing DC-area federal government employment. Second, I don’t think we have a national political consensus in support of creating new federal government programs with large employment impacts in the capital region. Third, I do think the effort by congressional democrats to increase taxes right now is one that carries with it significant political risk for the only political party that has any business being in control of the White House or the Capitol –January 6th happened so let’s just leave it there.

On a County budgetary level, it is a mixed bag. Obviously, inflation makes debt service costs cheaper – that’s a plus. There are likely to be some benefits related to home price inflation that will get passed through property tax valuations and transfer & recordation tax revenues. Furthermore, there are several related upward pressures on income tax revenue including: the stock market topping out, wage and salary inflation leading to higher incomes for working residents, and congressional push to increase the capital gains tax retroactively. On the other hand, not only is the County spending more on specific goods, but the cost of labor (80%-ish of County spending) and retirement benefits for former employees are also likely to increase. My guess is that the impacts on labor and retirement costs are much more likely to stay with us than the revenues, so this does create some fiscal risk over the longer-term that will erode the benefit of our existing debts getting cheaper.

CONSTRUCTION IMPACTS OF INFLATION

I’ve been keeping an eye on construction costs – while they are a lot higher than they were a year ago, the increases have stabilized a bit over the past couple of months.

The Producer Price Index for materials and components for construction is up 19% over the past 12 months, though the rate of inflation peaked in June and has been coming back down since then. The cost of specific inputs have soared this year, including: plywood, hardwood lumber, asphalt, and plastic construction products. Ed Zarenski, a construction economist, estimates that inflation in lumber prices alone has led to a $17,000 increase since mid-April in the cost of constructing a new home.

Producer prices have generally been increasing faster than final prices, suggesting that margins are shrinking. Typically, this would mean that fewer and fewer projects are financially feasible. As a result, it is possible that the numerous bidders for a relatively small number of projects could lead to some cost savings for general contractors at the expense of subcontractors. I’ll be keeping an eye on this potential trend – the interplay of materials cost inflation, financial feasibility of projects, and margins for both general contractors and subcontractors in the construction industry. In any event, my assumption is that building materials cost inflation is likely to recede to some degree as specific bottlenecks clear.

LABOR FORCE

For Maryland, the number of people in the labor force has declined by about 208,000 since January of 2020. On average during the past decade, the labor force has grown by about 22,000 per year. Taken together, this means that there are nearly 250,000 fewer workers in Maryland’s labor force today than there would have been if we had continued our pre-pandemic trajectory. That’s a pretty big number. And the monthly flows do provide some insights – while the labor force shrank by 191,000 over the 12 months ending with January 2021, the lion’s share of that decline occurred can be traced to the end of summer and start of the school year. In fact, the monthly decline from August 2020 to September 2021 was 152,000. As we look ahead to this fall, the August to September 2021 change in the labor force will be among the most important datapoints to watch. That data will be released October 22 for Maryland and November 3 for the County.

EMPLOYMENT

One piece of good news in the most recent Current Employment Survey is that while total private employment in Maryland grew by only 1,400 from July to August, employment in the Scientific Research and Development Services industry increased by 1,500. That is an industry in which a lot of the Maryland jobs are based in Montgomery County.

However, I imagine that whatever good news we see in the Science Research and Development Services industry will be swamped by the expected seasonal and pandemic related declines in Leisure and Hospitality. Whether you are looking at the seasonally adjusted numbers or not, a significant chunk of the recent rebound has been centered in that industry. As with the labor force data, we’re looking at mid-October and early November releases for the Maryland and Mo Co numbers.

That’s it for now! Be safe out there, shop Mo Co, and just generally try to be a good human.